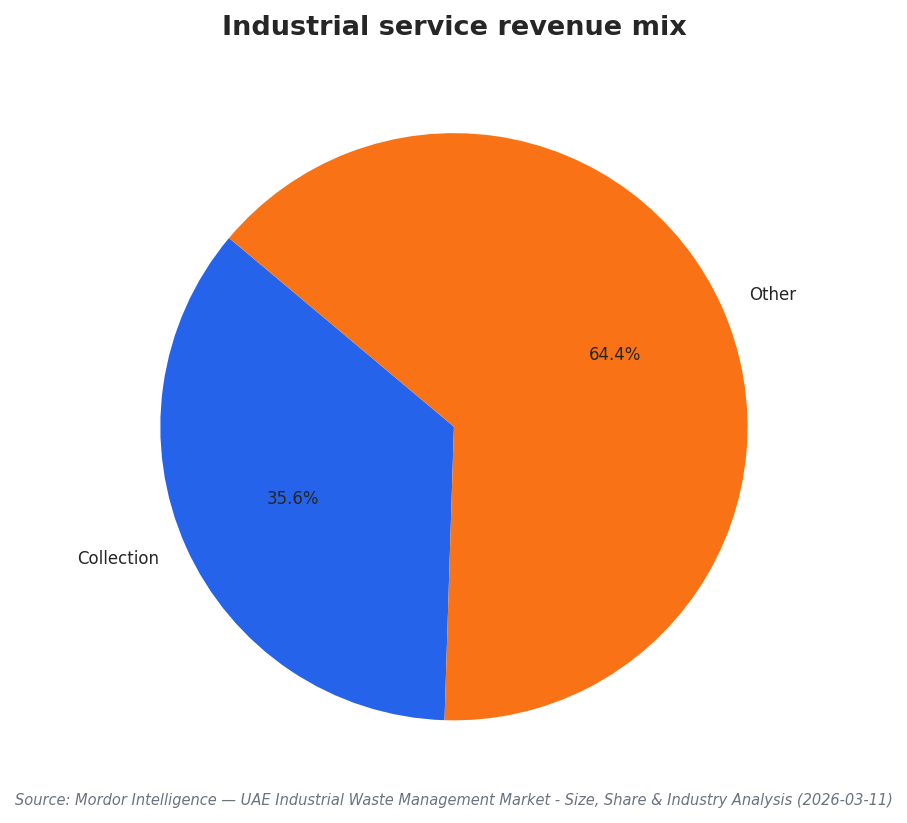

Abu Dhabi’s push toward a circular economy is being shaped by stricter diversion goals, new compliance tools, and continued investment in treatment options. Across the UAE’s industrial waste landscape, Mordor Intelligence estimates the market at USD 4.09 billion in 2025, rising from USD 4.36 billion in 2026 to USD 6.01 billion by 2031 at a 6.61% CAGR. In 2025, collection led services with a 35.6% revenue share, while recycling and material recovery is forecast to grow at a 7.91% CAGR through 2031. These shifts frame the Abu Dhabi waste management market as one that is moving beyond collection, but still has clear execution gaps.

Infrastructure and process constraints remain a recurring theme in the sources, especially where sorting, recovery, and consistent feedstock are needed. Ken Research states that existing UAE facilities struggle to handle increasing waste volume projected to reach 12 million tons in future, and it also notes that only 60% of waste is collected and processed effectively. The same source says the potential to recycle an additional 2 million tons annually could significantly impact the market, and mentions recycled materials volume rising to 1.2 million tons in future. Separately, Grand View Research highlights that Dubai and Abu Dhabi are actively investing in waste-to-energy projects and modern landfill sites, while also noting high capital investment for treatment facilities and waste-to-energy plants as a key restraint.

Recycling Infrastructure: Policy Pull Meets Real-World Bottlenecks

Policy and enforcement are increasingly designed to route waste into licensed pathways, which can strengthen recycling economics if capacity exists. Mordor Intelligence points to pilot EPR schemes launched in July 2025, requiring brand owners to fund post-consumer collection, with diversion quotas rising from 30% in 2026 to 60% by 2030. It also notes a January 2026 VAT reverse-charge rule that formalizes scrap trading and tightens audit trails, plus digital tools such as Tahweel’s national recyclables exchange to improve price discovery for smaller collectors. However, a Saudi Arabia-focused ScienceDirect review offers a cautionary parallel: it describes a gap between high-level infrastructure expansion and underdeveloped supply chains needed for consistent feedstock generation, alongside inadequate infrastructure for waste sorting and delays tied to overlapping responsibilities.

Construction and demolition waste is another pressure point where circular outcomes depend on both rules and processing throughput. Mordor Intelligence estimates the UAE construction and demolition waste management market at USD 1.05 billion in 2025, growing from USD 1.11 billion in 2026 to USD 1.47 billion by 2031 at a 5.90% CAGR. In that segment, recycling and material recovery led with a 39.7% share in 2025, and concrete and bricks held a 69.0% material share. Ken Research adds that high initial investment costs can be prohibitive, often exceeding AED 5 million for small to medium-sized enterprises setting up recycling facilities. This cost barrier can translate into localized investment gaps, even as major cities like Dubai and Abu Dhabi dominate activity due to construction volumes.

Closing investment gaps in Abu Dhabi’s circular economy will likely depend on aligning compliance, financing, and end-market demand for recovered materials. In industrial waste, landfill still captured 54.35% of 2025 volumes in the UAE, even as incineration and energy recovery is projected to grow at an 8.51% CAGR to 2031, according to Mordor Intelligence. The same report notes that Bee’ah, Tadweer, and Veolia controlled about 40% of 2025 revenue, suggesting scale advantages for operators with sorting or thermal assets. Ken Research also reports the UAE government allocated AED 1.5 billion (about USD 408 million) for waste management projects. For Abu Dhabi, the practical challenge is turning investment and rules into consistent sorting, reliable feedstock, and profitable recovery pathways that keep material out of landfill.

What is driving growth in Abu Dhabi’s waste management market outlook?

What infrastructure gaps are highlighted for recycling and circular economy progress?

How do EPR rules connect to recycling performance?

Why can investment be difficult for smaller recycling operators?